What is the Income Statement?

One of a business’ most important financial statements, the Income Statement details the company’s earnings and expenses for a certain accounting period. A profit or loss is calculated by deducting all operating and non-operating expenditures from total revenues.

In corporate finance (which includes financial modeling) and in accounting, the income statement is one of three statements utilized. The statement organizes the company’s financial data in a comprehensible fashion, detailing its revenue, costs, gross profit, selling and administrative expenditures, other expenses and income, taxes paid, and net profit.

Each section of the statement covers a distinct time frame that corresponds to an essential aspect of the company’s activities. For internal purposes, monthly periods are used most often, however some businesses employ a thirteen-period cycle. We sum the figures reported in these reports every three months to get our yearly report.

Due to its minimal data requirements from the income statement, balance sheet, and cash flow statement, this statement is an excellent starting point for any financial model. This means that the income statement comes first in the chain of financial statements since it contains the most information.

Components of an Income Statement

Due to the fact that a company’s income and expenditures will vary based on the nature of its operations, the income statement may range slightly from one firm to the next. However, most income statements will include a few standard sections.

Here are some of the most typical categories included in an income statement:

Revenue/Sales

Revenue from Sales is the top line of a profit and loss statement and represents money brought in by the business via the sale of goods or provision of services. This sum will include all upfront expenses incurred in bringing a product or service to market. Multiple sources of income are combined to form a company’s top line in some businesses.

Cost of Goods Sold (COGS)

The direct expenses incurred by a business in order to make a profit from selling their products are summed up in a line item called “Cost of Goods Sold” (COGS). If the organization provides a service, this line item may also be referred to as Sales Expenses. Direct costs include things like labor, components, materials, and a portion of things like depreciation that are directly related to the production of the good or service (see an explanation of depreciation below).

Gross Profit

Gross Profit Gross profit is calculated by subtracting Cost of Goods Sold (or Cost of Sales) from Sales Revenue.

Marketing, Advertising, and Promotion Expenses

All businesses have costs that arise from selling their products or services. Because of their similarities and because they all have to do with making a sale, marketing, advertising, and promotion costs are sometimes lumped together.

General and Administrative (G&A) Expenses

All other non-direct costs of doing business go under the heading of “selling, general, and administrative,” or “SG&A.” Expenses like payroll, rent and utilities for an office space, insurance premiums, transportation costs, and even depreciation and amortization are all part of running a business. However, businesses can choose to report depreciation and amortization separately if they so want.

EBITDA

EBITDA, which stands for Earnings before Interest, Tax, Depreciation, and Amortization, is a metric that is not included in every income statement. It’s the amount left over after deducting the cost of selling, general, and administrative expenditures from the total revenue earned.

Depreciation & Amortization Expense

Accountants construct depreciation and amortization as non-cash expenditures to write down the initial investment in capital assets like PPE over time (PP&E).

Operating Income (or EBIT)

Operating Income is the money brought in by running the firm normally. Put another way, it’s the net gain after revenues have been adjusted for factors like interest and taxes but before any non-operating income or costs have been deducted. Earnings before interest and taxes (abbreviated as “EBIT”) is a frequent financial phrase.

Interest

Cost of Interest. When analyzing a company’s financial performance, it is usual practice to display interest revenue and interest expenditures in their respective sections of the income statement. It’s done this this to square away the gap between EBIT and EBT. The debt schedule is the basis for calculating interest expenditure.

Other Expenses

Other, more specialized costs might arise for businesses. Fulfillment costs, IT costs, R&D costs, stock-based compensation costs, impairment charges, investment sale gains/losses, currency fluctuations, and many other expenditures are possible.

EBT (Pre-Tax Income)

Pre-tax income, or Earnings Before Tax, is calculated by deducting interest costs from operating income. Before calculating net income, this is the last category to add up to.

Income Taxes

When discussing taxes, “income taxes” refer to those levied against after-tax earnings. Total tax cost may include both presently due taxes and those that are projected to become due in the future.

Net Income

After subtracting federal, state, and local taxes from gross revenue, we arrive at net income. After dividends are subtracted, this is the amount that moves into retained profits on the balance sheet.

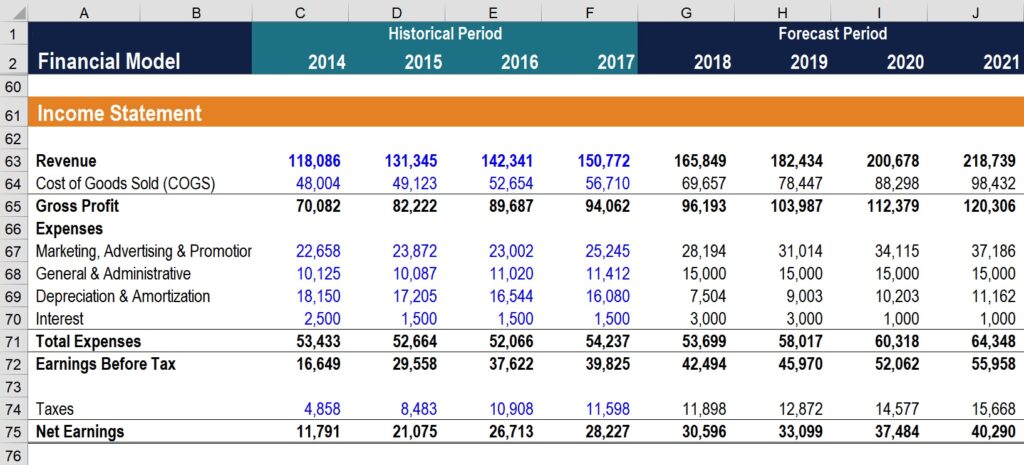

A Real Example of an Income Statement

The financial statements (income statements) for the years 2015–2017 that Amazon has consolidated are displayed here. See the profit and loss statement and get the details down below.

To begin, we can observe that Amazon generates income from the sale of both physical goods and digital services.

As the cost of sales is bundled in with other expenditures such as fulfillment, marketing, technology, content, general and administration (G&A), and other expenses, there is no gross profit subtotal.

Finally, after subtracting all of these costs, we have what is called “Operating Income” on the income statement (also known as EBIT or Earnings Before Interest and Taxes).

Non-operating expenditures, the income tax provision (i.e., future taxes), and equity-method investment activity (profits or losses from minority investments), net of tax, are examples of items that fall below Operating Income that are unrelated to the normal course of business.

When we have the net income (or net loss), we can divide that number by the diluted weighted average number of shares outstanding to get EPS (EPS).

How to Build an Income Statement in a Financial Model

Once the bones of an income statement have been laid out, they may be included into a robust financial model to make projections about the company’s future success.

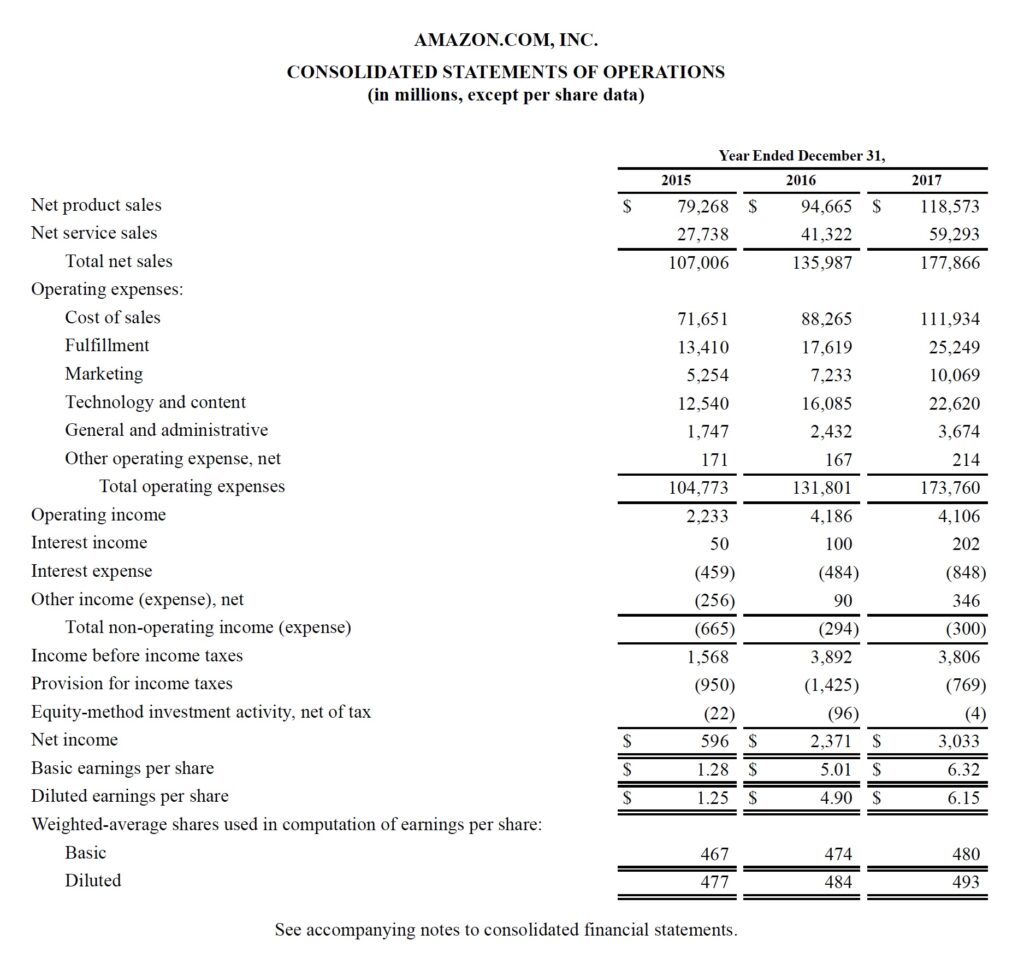

Step 1

To begin, use the Excel income statement template to record past financial results for whatever time frame that you have access to. If you want to tell the difference between hard-coded and computed data, you need use a certain format when entering historical data. To refresh your memory, blue is often reserved for hard-coded input whereas black is used for calculated or linked data in this type of format.

By doing so, both the user and the reader will be aware of which cells contain equations and thus should not be altered and which cells are for input only. However, consistency in use is essential to minimize misunderstanding, so use whichever approach you choose for formatting.

Step 2

The next step is to conduct trend analysis on the existing historical data in order to develop forecasting drivers and assumptions. Using data like sales growth rates and cost of goods sold percentages, you may make educated predictions about the future. Study up on various methods of prediction.

Step 3

Finally, anticipate future values for each line item in the income statement using the drivers and assumptions you established in step one. You may use your predictions for individual line items to determine individual subtotals. Gross profit forecasting, for instance, is more accurate if one first predicts Cost of Goods Sold and Revenue, and then subtracts these two figures.

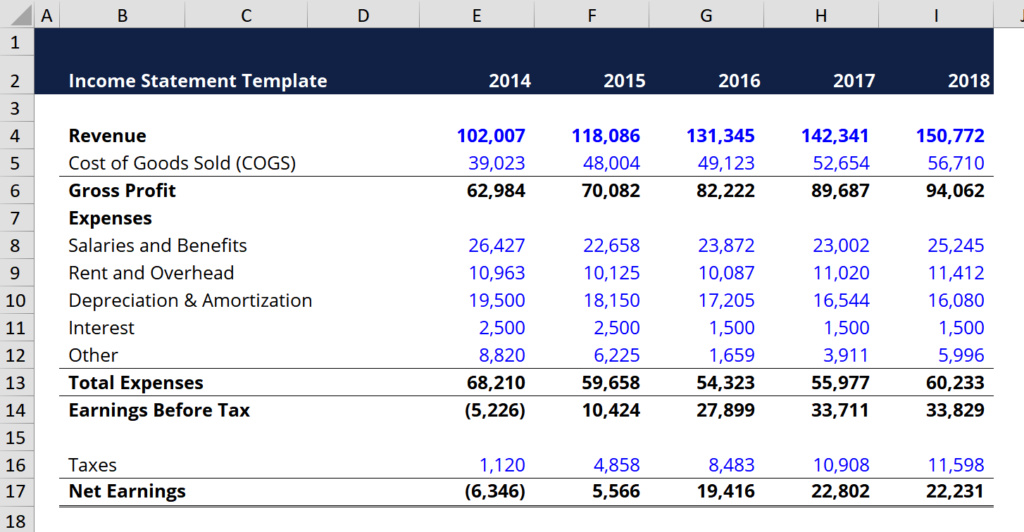

Income Statement Template

Please download free income statement template to produce a year-over-year income statement with your own data.

What are Common Drivers for Each Income Statement Item?

| Line Item | Driver or Assumption |

|---|---|

| Sales Revenue | Selected growth percentage, pegged growth percentage based on index (such as GDP) |

| Cost of Goods Sold | Percentage of sales, Fixed dollar value |

| SG&A | Percentage of sales, fixed amount, trend, fixed dollar value |

| Depreciation and Amortization | Depreciation Schedule |

| Interest Expense | Debt Schedule |

| Income Tax | Percentage of pre-tax income (effective tax rate) |

Commonly used though they may be, the drivers discussed here should be seen as little more than suggestions. Intuition is needed for some times to select the right driver or assumption to apply. A company may generate no income, as one example. That means it’s impossible to calculate COGS based on the percentage of sales drivers. Instead, the analyst might have to make estimates about future COGS by looking at historical trends.

Financial modeling and accounting both rely on the same fundamental statements. There are three financial statements: the Income Statement, Balance Sheet, and Cash Flow Statement. All of the other statements’ values will be affected by the ones you choose in this list, because they all form part of the same financial model.